- Global additions grow 45% year-on-year

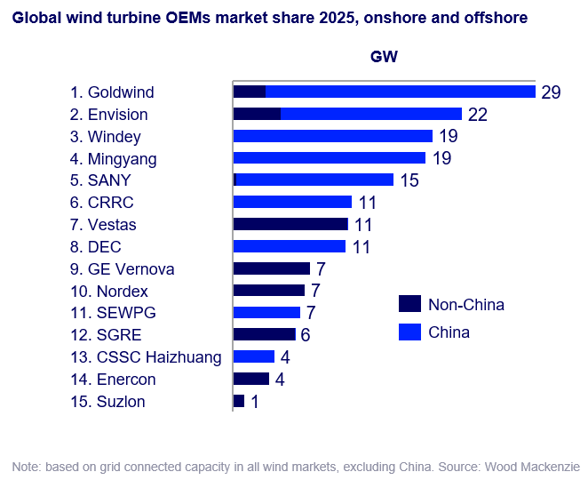

- Goldwind and Envision exceeded 20 GW of installations

- China becomes the first country to exceed 100 GW

Wood Mackenzie's latest analysis 'Global wind turbine OEMs 2025 historical market share' reveals the global wind industry delivered 176 GW of new capacity in 2025. This represents a 45% year-on-year increase and marks the strongest annual growth on record. China accounted for the majority of new additions. The country became the first market ever to surpass 100 GW of wind installations in a single year, driven by strong provincial targets and the shift to market-based pricing.

'Outside China, installations grew 22%, supported by strong activity across Asia Pacific, Europe, North America and emerging regions in Africa and Central Asia,' said Endri Lico, principal analyst at Wood Mackenzie 'Latin America was the only region to contract. Wind deployment expanded globally, with more than 60 countries connecting new capacity in 2025, a 13% increase from the prior year. China, the United States, India and Germany remained the largest individual contributors by volume.'

Chinese turbine makers dominate global rankings with record overseas expansion

Chinese turbine manufacturers had a standout year in 2025, filling the top six positions in the global ranking. Nine Chinese OEMs achieved record deliveries. Total overseas installations by Chinese OEMs reached 8.5 GW across 22 markets, more than triple their 2024 level. Growth concentrated in emerging markets where competitive pricing and faster delivery cycles helped Chinese suppliers expand market reach.

Goldwind and Envision led the pack. For the first time, two turbine manufacturers exceeded 20 GW of installations. Their momentum reflects a strategic model rooted in scale, competitive pricing and rapid deployment. China's substantial domestic buildout and expanding presence in emerging markets support this approach.

This approach contrasts sharply with Western manufacturers, who deliberately narrowed focus to core, higher-margin markets. Western OEMs emphasise platform simplification, pricing discipline and operational stability. Both strategies proved effective in 2025.

Western OEMs maintain dominance outside China

Despite reduced global share, Western OEMs remained the dominant suppliers in markets outside China. They secured 75% of ex-China installations and supplied turbines to almost 50 different countries, an all-time high. Vestas continued to hold the broadest international footprint, delivering turbines in almost 40 markets in 2025. This demonstrates that multiple strategic approaches can succeed simultaneously in the global wind market.

'2025 marked a pivotal year, with both Chinese and Western OEMs delivering strong outcomes through distinct strategic approaches,' said Lico. 'Chinese and Western OEMs are succeeding through fundamentally different strategies — one built on scale and expansion, the other on selectivity and profitability. This divergence highlights a pluralistic industry landscape, where multiple models can coexist effectively.'

India rebounds as domestic manufacturers regain momentum

India recorded a strong rebound in 2025 as domestic installations nearly doubled. Domestic players connected 2.7 GW. Suzlon returned to the global top 15, and other Indian OEMs secured top ten positions outside China. This resurgence demonstrates the continued viability of regional manufacturers in their home markets when supported by favourable policy conditions and growing electricity demand although Chinese OEMs will continue to challenge their position.

Technology strategies diverge but remain aligned on platform scaling

Technology development also reflects this strategic divergence. Chinese manufacturers pushed ahead with super-sized onshore rotors above 200 metres. They advanced early deployments of 16–18 MW offshore turbines. Western OEMs, in contrast, focused on extending proven platforms, optimising rotor diameters and progressing 15 MW-class offshore models. These models align with permitting and grid constraints in their core markets.

However, despite these differences, both groups shared one fundamental approach. They built their 2025 portfolios by scaling established turbine platforms, not by introducing new product families. The industry's technology progression diverged in pace and emphasis. It remained unified in direction — refining and tailoring existing designs rather than shifting to entirely new architectures.

'Looking ahead, we expect this dynamic to continue, with turbine manufacturers pursuing differentiated strategies tailored to their core markets,' added Lico. 'For Western OEMs, this will increasingly involve introducing new turbine variants before the end of the decade built on existing platforms to drive cost reductions. This pragmatic evolution underscores an industry that is steadily maturing, with a sharper focus on operational efficiency and long-term financial sustainability.'

Source: Wood Mackenzie